Worried about crossing the tax threshold when self-employed?

If you’ve started working for yourself, understanding tax can feel like a minefield. Many new freelancers worry about exactly when they need to start paying tax and what their obligations are.

As a self-employed individual, you are responsible for calculating and paying your own self employed income tax and National Insurance contributions.

It’s a common question: “How much can I earn before HMRC wants a slice of my income?” The good news is that the tax-free threshold might be higher than you think, though there are different rules for registration versus actually paying tax.

Let’s break it down in simple terms so you know exactly where you stand with your self-employed income and tax responsibilities.

If you'd like help with adding your income and expenses correctly or need support understanding your tax obligations, we're here to guide you every step of the way.

Understanding Self Employment Tax

Self-employment tax refers to the tax obligations of sole traders and freelancers. As a self-employed individual, you are responsible for calculating and paying your own income tax and National Insurance contributions.

This can be a significant adjustment for those transitioning from employee to self-employed status. It’s crucial to understand that income tax and National Insurance contributions are payable on your profits, not your total income. To determine your taxable profits, you need to deduct allowable business expenses from your self-employed income.

This means that careful record-keeping and understanding what expenses you can claim are essential to managing your self-employment tax effectively.

How much do you have to earn to pay tax when self-employed?

The magic number most people need to know is £12,570. This is your Personal Allowance for the 2024/25 tax year, and any income you earn up to this amount is completely tax-free.

Once your income exceeds the Personal Allowance, you will need to pay self employment tax on your profits.

However, there’s an important distinction to make. Just because you don’t have to pay tax doesn’t mean you can ignore HMRC altogether. You need to register for Self Assessment once your self-employed income exceeds £1,000 in a tax year, known as the Trading Allowance.

National Insurance works differently too. Self-employed people pay Class 2 and Class 4 National Insurance once profits reach certain thresholds. For the 2023/24 tax year, you’ll start paying National Insurance when your profits reach £12,570 – the same as the Personal Allowance threshold.

Tax Free Personal Allowance

The tax-free personal allowance is the amount of money you can earn without paying income tax. For the 2024/25 tax year, the standard personal allowance is £12,570.

This means that if your profits are below £12,570, you won’t pay income tax. However, you may still need to pay National Insurance contributions. If you have other sources of income, such as employment income, you may need to pay income tax on your total income.

It’s important to consider all your income sources when calculating your tax obligations to ensure you’re not caught off guard by an unexpected tax bill.

How does National Insurance work when you're self-employed?

When you’re self-employed, you pay two types of National Insurance: Class 2 and Class 4. Class 2 contributions are currently a flat weekly rate that you pay if your profits are £12,570 or more per year.

Class 4 contributions are percentage-based. You pay 9% on profits between £12,570 and £50,270, and 2% on anything above that. These contributions count towards your State Pension and other benefits, so they’re important to keep up with.

You pay both Income Tax and national insurance through your self-assessment tax return, usually by 31st January each year. Filing your assessment tax returns accurately and on time is crucial to avoid penalties and ensure you meet your tax obligations. Many of my clients find this aspect of self-employment particularly confusing at first, but it becomes routine after the first year.

What if I have a job and self-employment income?

If you're employed and self-employed at the same time, your tax situation gets a bit more complex. Your Personal Allowance of £12,570 applies to your total income from all sources, with your employer already using some of this allowance for your PAYE income.

Let's say you earn £10,000 from your job. This leaves £2,570 of your Personal Allowance for your self-employed work before you start paying tax on it. You'll still need to register as self-employed and complete a Self Assessment if your self-employed income exceeds £1,000.

Remember that having multiple income sources might push you into a higher tax band sooner than you expect. It's worth calculating your total expected income to avoid surprises when your tax bill arrives.

How can I reduce my self-employed tax bill?

The most straightforward way to reduce your tax bill is to claim all legitimate business expenses. These reduce your taxable profit and include things like office costs, travel expenses, phone bills, and professional subscriptions related to your work.

Working from home? You can claim a proportion of your household bills or use HMRC's simplified flat rate. Pension contributions are another tax-efficient way to reduce your bill, as they receive tax relief at your highest rate of Income Tax.

The key is keeping good records of all your income and expenses. This makes completing your tax return much easier and ensures you don't miss out on any tax relief that could significantly reduce what you owe.

Common mistakes to avoid with self-employed tax

Not setting aside money for tax throughout the year is probably the biggest mistake new freelancers make. That tax bill can come as a nasty shock, especially when combined with payments on account – advance payments towards next year's tax bill.

Missing the Self Assessment deadline (31st January) results in an immediate £100 fine, with further penalties the longer you delay. Another common error is not claiming all the expenses you're entitled to, meaning you pay more tax than necessary.

Many self-employed people don't realise they need to register even if they're below the tax-paying threshold but above £1,000 in income. This misunderstanding can lead to penalties that could easily have been avoided with proper registration.

Business Structures and Tax

The structure of your business significantly affects your tax reporting requirements and deadlines. As a sole trader, you’ll need to complete a Self Assessment tax return annually. If you operate as a limited company,

you’ll be required to pay Corporation Tax on your profits and adhere to different reporting standards. Partnerships and other business structures have their own unique tax reporting requirements.

Understanding your business structure and its tax implications is crucial to ensure you meet all your tax obligations and avoid any penalties. It’s often beneficial to seek professional advice to navigate these complexities effectively.

State Pension and Self Employment

As a self-employed individual, you may be eligible for a state pension, but your National Insurance contributions will play a crucial role in determining your entitlement. If you’re making voluntary National Insurance contributions, you may be able to increase your state pension entitlement.

It’s essential to understand how your self-employment affects your state pension and to seek advice from a professional advisor if needed. Ensuring you make the necessary contributions can help secure your financial future and provide peace of mind.

Tax Rates and Thresholds

Tax rates and thresholds determine how much income tax you’ll pay. For the 2024/25 tax year, the income tax rates are as follows:

- 20% on profits between £12,571 and £50,270

- 40% on profits between £50,271 and £125,140

- 45% on profits above £125,140

National Insurance contributions are also payable on your profits. Class 2 National Insurance contributions are £3.15 per week for self-employed individuals making between £6,725 and £9,880 in profit. Class 4 National Insurance contributions are 9% of profits between £9,880 and £50,270, and 2% on profits above £50,270. Understanding these rates and thresholds is essential for accurate tax planning and ensuring you set aside enough money to cover your tax obligations.

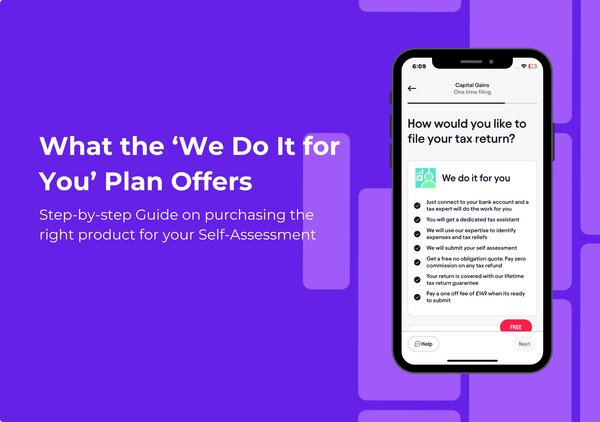

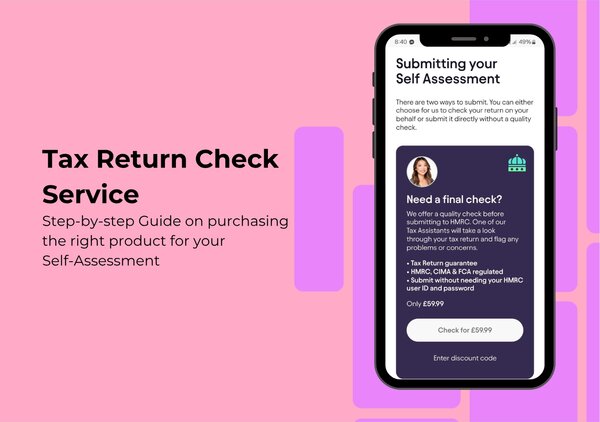

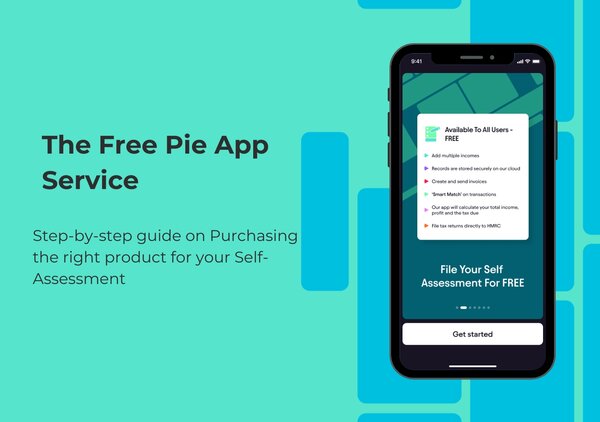

Make your self-employed tax life easier

Understanding exactly when and how much tax you will pay. helps you plan your finances better as a self-employed person. Remember the key thresholds: register once you earn over £1,000, and you'll start paying Income Tax when your total income exceeds £12,570.

Keeping organised records throughout the year will save you stress when it's time to file your tax return. If you're finding tax management challenging, consider using dedicated tools designed for self-employed individuals.

Pie is the UK's first personal tax app designed specifically for working individuals. It offers integrated bookkeeping, real-time tax figures, and simplified tax return processing to take the headache out of self-assessment. Why struggle with complicated tax matters when there's a simpler way?

Quick and Easy Guide to Add Self Employed Income

Follow these steps to add self emploment income in the Pie app

Add your income by swiping right on any taxable income you want to declare on your tax return. This will move the transaction into the ‘income tab’.Step 1

Use the ‘Quick Add’ feature to manually enter any additional income or expenses not found in your bank transactions for your self-assessment.Step 2