To the point

Many UK high earners assume that because their employer handles their tax through PAYE, they’ve fulfilled all their tax obligations. Unfortunately, this isn’t always the case.

Most taxpayers who are taxed at source through PAYE do not need to file a Self Assessment tax return, but high earners may have additional obligations.

Additional income sources often trigger Self Assessment requirements, even when you’re paying tax through PAYE. High income itself can create filing obligations even if your finances seem straightforward.

HMRC penalties for failing to file can be substantial and may apply retrospectively for several years. This can lead to unexpected tax bills and stress that could have been avoided.

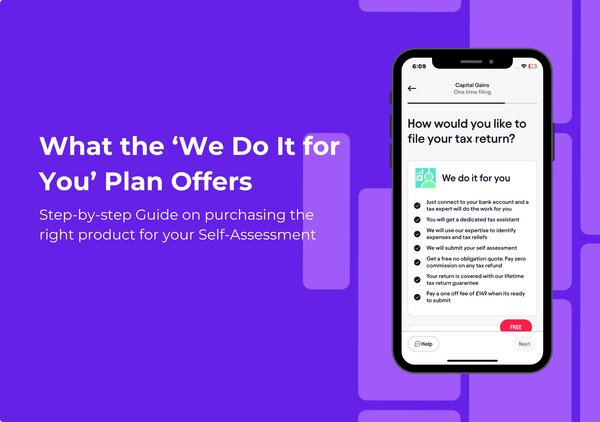

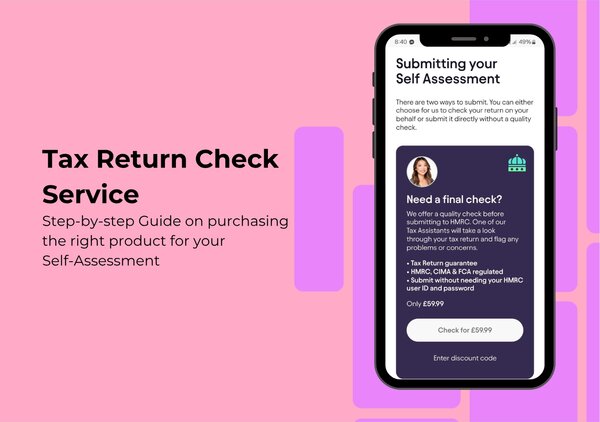

Pie, the UK’s first personal tax app, can check your filing requirements in minutes and handle your Self Assessment hassle-free. Or if you’re just here to get to grips with it all, let’s break it down!

What Triggers Self Assessment for PAYE Employees?

Several situations require PAYE employees to file a Self Assessment tax return. Understanding these triggers can save you from costly mistakes.

Income over £100,000 automatically triggers the need for Self Assessment, regardless of how simple your tax affairs might be. The income threshold for self assessment is currently £100,000, but this threshold may change in future tax years.

When calculating whether you exceed the income threshold, you must include your total employment income as well as any additional income. Additional income exceeding £1,000 from property, investment income, freelance work, or other income such as untaxed earnings from side jobs means you’ll need to file. This applies even if tax has been deducted at source on some income.

Certain benefits and expenses that aren’t fully taxed through your payroll system require declaration. Higher-rate taxpayers claiming pension tax relief or significant charitable donations often need to file.

Being a company director typically necessitates Self Assessment, even if your only income is from PAYE. This requirement catches many professionals by surprise.

Do High Earners Need to File a Self Assessment if They Already Pay PAYE?

For tax purposes, HMRC defines a high earner as someone whose income exceeds specific thresholds. If you earn over £100,000 a year, you are considered a high earner and must file a Self Assessment tax return, even if you pay tax through PAYE. This is a clear HMRC requirement with no exceptions.

High earners may need to file a tax return or submit a Self Assessment tax return even if they do not owe tax. The obligation to submit applies if your income is above the threshold, or if you have additional income sources, regardless of whether you owe tax at the end of the year.

Failing to register and file when required can result in penalties, even if you don’t owe any additional tax. HMRC’s penalties are designed to encourage compliance, not just collect unpaid tax. The income threshold for mandatory assessment tax returns was recently increased from £100,000 to £150,000 and then removed altogether for the 2024/25 tax year, changing the filing requirements for high earners.

Additional Income Sources Requiring Declaration

Rental property income must be declared, even if you’re using the property allowance. This applies whether you rent out a room or an entire property.

Dividends are a form of investment income that must be declared if they exceed the dividend allowance (currently £1,000). Many professionals with investments overlook this requirement.

Capital gains and other earnings from selling assets like shares or a second property require declaration if they exceed your annual exempt amount. The calculations can be complex and are best handled properly.

Money received from foreign sources often needs to be reported, even if you’ve already paid tax on it abroad. Double taxation agreements may apply, but you still need to declare the income.

Self employment income over £1,000 annually must be reported. This includes consultancy, speaking engagements, or writing work.

Benefits and Expenses That Trigger Filing

Company benefits not fully taxed through payroll need separate declaration. These might include private medical insurance or certain types of share options.

Private use of a company car often requires additional tax calculations. The benefit value depends on the car’s emissions and original list price.

Healthcare benefits, especially those exceeding standard allowances, may trigger filing requirements. This includes private medical insurance paid by your employer.

Expense claims that fall outside normal PAYE processing need separate reporting. Only allowable expenses those that can be deducted from your income to reduce taxable profit should be claimed. Examples include professional subscriptions or working-from-home expenses, but these must be reported separately from expenses processed through PAYE.

Share schemes and employee ownership arrangements typically require Self Assessment. These can create complex tax situations that PAYE cannot adequately handle.

Deadlines and Penalties for High Earners

You must register for Self Assessment by 5 October following the end of the tax year in which your income first exceeded £100,000. Missing this deadline can trigger the penalty process.

Paper returns must be submitted by 31 October following the end of the tax year. Online filing gives you until 31 January following the end of the tax year. Pension contributions made before the end of the tax year can reduce your taxable income and affect your tax liability, so be sure to report these contributions accurately.

Late filing penalties start at £100 and increase significantly the longer you delay. After three months, you’ll face daily penalties of £10 up to a maximum of £900.

Interest and surcharges apply to late payments, which can substantially increase your tax bill. HMRC currently charges interest at 7.75%, which adds up quickly on larger amounts.

The penalty regime is particularly strict for high earners, with potential penalties of up to 100% of the tax due in cases of deliberate non-compliance.

Self Assessment Process for PAYE Employees

First, register for Self Assessment through your Government Gateway account if you haven’t filed before. This process can take several weeks, so don’t leave it until the last minute.

Gather all income documentation, including your P60, P11D, bank statements, investment records, and statements from your pension provider. Organised record-keeping makes the process much smoother.

Complete your tax return either online or using tax software before the relevant deadline. The online system will guide you through the sections relevant to your situation.

Pay any additional tax due by the payment deadline (usually 31 January). Consider whether you’ll need to make payments on account for the following tax year.

Setting up a reminder system for key tax dates can help ensure you never miss a deadline. Most tax problems stem from missed deadlines rather than complex calculations.

Final Thoughts

High income brings additional tax responsibilities that go beyond standard PAYE arrangements. Understanding these obligations is part of effective financial management.

HMRC expects those earning over £100,000 or with additional income sources to engage with Self Assessment regardless of their PAYE status. The system is designed to capture income that PAYE might miss.

Taking proactive steps to understand and meet your filing requirements will save you stress and potential penalties down the line. Prevention is always better than cure in tax matters.

If you're uncertain about your specific obligations, seeking professional advice is always worthwhile. The cost of advice is typically far less than the cost of mistakes.

Pie: Simplifying High Earners' Self Assessment Tax

Managing your tax obligations shouldn't be stressful, even with a complex income situation. Pie was designed specifically for professionals who need clarity without complexity.

Our app offers real-time calculations specifically designed for professionals with multiple income streams, giving you clarity throughout the tax year. You'll always know where you stand.

Our high-income specialist tools help identify often-missed deductions that can reduce your tax bill beyond what PAYE calculations capture. Many users discover legitimate tax savings they weren't aware of.

We handle direct HMRC filing with built-in checks to ensure your return meets all requirements, preventing those unwanted penalty notices. Peace of mind comes as standard.

Why not explore the Pie app to see how we can simplify your tax life?