To the point...

Blockchain identity systems are transforming how we manage personal data, with significant tax implications for UK users and developers.

HMRC has begun clarifying how these technologies intersect with existing tax frameworks. The tax treatment varies significantly depending on whether you're using, developing, or investing in blockchain identity solutions.

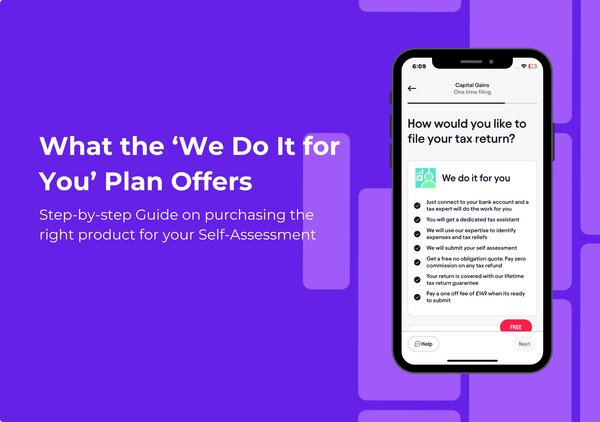

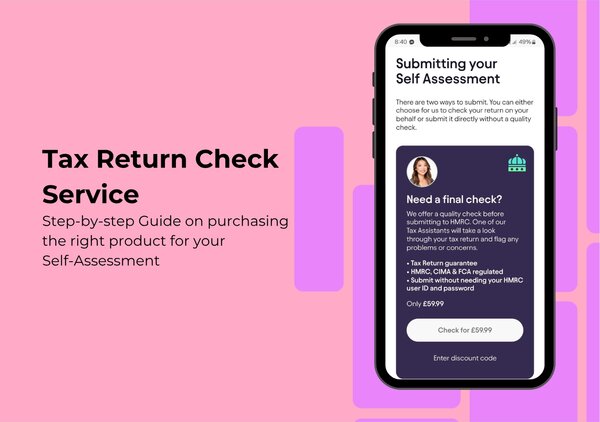

Understanding your obligations early can prevent costly compliance issues down the line. Our tax specialists at Pie tax, the UK's first personal tax app, have helped dozens of blockchain developers navigate these complex regulations. Or if you're just here to get to grips with it all, let's break it down!

What's the deal with blockchain identity tax?

Blockchain identity solutions create a digital fingerprint that proves who you are without revealing all your personal details. But how does HMRC view these systems for tax purposes?

When you use blockchain for identity verification, you might be creating taxable events without realising it. This is especially true if tokens or cryptocurrencies are involved in the process. HMRC treats different aspects of blockchain identity differently. Using a blockchain ID system for personal purposes generally has minimal tax impact.

Developing or investing in these solutions, however, can trigger various tax obligations. The line between personal use and commercial activity can get blurry fast. For example, if you're earning rewards for participating in a blockchain identity network, HMRC might view this as taxable income.

Key tax obligations for blockchain identity developers

If you're building blockchain identity solutions in the UK, corporation tax will apply to your profits at the current rate of 25% for most businesses.

VAT considerations are tricky blockchain identity services might qualify as digital services under VAT rules. This requires registration once you hit the £85,000 threshold.

The innovative nature of blockchain identity work means you might qualify for R&D tax relief. This could potentially reduce your tax bill by up to 33p for every £1 spent on qualifying activities.

When hiring developers for your blockchain identity project, remember that PAYE and National Insurance contributions apply. These work just as they would for any tech role.

I recently advised a London startup that saved over £40,000 through R&D claims on their blockchain identity platform. Their innovative approach to zero-knowledge proofs qualified as genuine technological advancement.

Tax treatment for blockchain identity investors

Investing in blockchain identity tokens or projects typically falls under Capital Gains Tax rules. This applies when you sell or exchange your investment at a profit.

The annual tax-free allowance for capital gains has reduced to £3,000 for 2023/24. This makes it more important than ever to track your blockchain investments carefully. If you're staking identity tokens or earning rewards for network participation, HMRC will likely view these as income rather than capital gains.

Keeping detailed records of acquisition dates, costs, and disposal proceeds is essential. Without these, accurate tax reporting of blockchain identity investments becomes nearly impossible.

Using blockchain identity: individual tax considerations

For most individuals, simply using a blockchain identity solution for personal verification won't trigger tax obligations.

However, if you're receiving tokens or other benefits for using or promoting these systems, these could be taxable. HMRC may classify them as income or capital gains.

Privacy-focused blockchain identity solutions can create tension with HMRC's record-keeping requirements. You'll need to balance privacy with sufficient documentation for tax compliance.

If you're using blockchain identity for business purposes, different rules may apply compared to personal use. This potentially affects allowable expenses and VAT recovery.

Cross-border tax issues with blockchain identity

The borderless nature of blockchain identity solutions creates complex international tax scenarios. This is especially relevant around permanent establishment rules.

When your blockchain identity business operates across multiple countries, you might face double taxation risks. These require careful navigation of tax treaties.

Digital services taxes are emerging in many countries, potentially affecting blockchain identity providers. These may apply if you serve users in those jurisdictions.

VAT "place of supply" rules determine where you need to register and charge VAT. For B2C digital services, this is usually where your customer is located.

Final Thoughts

Blockchain identity technologies present novel tax challenges that require careful navigation. HMRC continues to evolve its approach, making it essential to stay informed about guidance updates.

Professional tax advice is particularly valuable in this rapidly developing area. This is especially true where precedents are still being established. Pie is the first uk tax app that can help with the Blockchain tools to make th data safe.

Proper documentation of your blockchain identity activities is your best protection. It safeguards against future tax complications that might otherwise arise.