Let’s break it down!

Navigating UK cryptocurrency tax rules can be confusing for both casual traders and serious investors. If you are a crypto investor someone who holds cryptocurrencies for long-term investment rather than frequent trading HMRC views crypto as assets subject to capital gains tax, not currency.

Different crypto activities trigger different tax obligations. When it comes to tax in the uk, it's important to understand the specific rules and reporting requirements for crypto transactions. Understanding when tax is due can save you from unexpected HMRC penalties.

Pie tax‘s crypto tax calculator helps you track all your transactions across exchanges automatically. Or if you’re just here to get to grips with it all, let’s break it down!

The Basics of UK Crypto Tax

Cryptocurrency taxation in the UK follows specific rules set by HMRC. You don’t pay tax simply for buying crypto, but what you do with it afterwards matters.

HMRC treats crypto as property, not money. This means most crypto activities fall under Capital Gains Tax rules rather than Income Tax. In the UK, crypto taxed under these rules is generally treated similarly to stocks, with Capital Gains Tax applying to disposals and specific events.

You’ll need to track each transaction’s value in pounds sterling at the time it occurred. HMRC requires you to use the market value or fair market value of the crypto asset in fiat currency (GBP) at the time of each transaction to determine gains or losses. This becomes crucial when calculating your gains or losses.

Classification of Cryptocurrency for Tax Purposes

In the UK, HMRC classifies cryptocurrency as an asset rather than a currency for tax purposes. This distinction is crucial because it determines how your crypto activities are taxed. When you sell, trade, or otherwise dispose of your crypto assets, you are typically subject to capital gains tax. This means you need to pay capital gains tax on any profit you make from selling or exchanging your crypto.

However, if you receive cryptocurrency as payment for goods or services, or as a reward from mining or staking, this is treated differently. In these cases, you may need to pay income tax on the value of the crypto received, as it counts as taxable income. Understanding whether your crypto activity is subject to capital gains or income tax is essential for ensuring you pay the correct amount of tax and remain compliant with HMRC’s tax purposes.

When Do You Pay Tax on Crypto in the UK?

You pay tax when you “dispose” of your crypto assets. This includes selling for pounds, trading for another cryptocurrency, or using crypto to pay for goods. Activities such as selling crypto, when you sell crypto assets, or if someone sells crypto assets, are all considered disposals for tax purposes.

Giving crypto as a gift also counts as a disposal for tax purposes. However, simply holding crypto without selling doesn’t trigger any tax liability.

The UK tax year runs from 6 April to 5 April the following year. Gains and losses from crypto transactions must be reported within the same tax year, and tax returns must be filed accordingly.

If your total gains from all assets exceed the Annual Exempt Amount (£3,000 for 2023/24), you’ll need to report this on a Self Assessment tax return. You may owe capital gains tax on your taxable gains, and you are required to pay taxes by paying tax on any taxable gain above the allowance. If you owe tax, you must report and pay it to HMRC.

Income Tax on Cryptocurrency

Not all crypto activities fall under Capital Gains Tax. Some are subject to Income Tax instead.

Mining rewards, staking income, and payment for services in crypto are typically taxable as income. These may be classified as trading income, miscellaneous income, or employment income, and are subject to income tax rates and national insurance or national insurance contributions as applicable. The rates depend on your income band: 20% for basic rate, 40% for higher rate.

Tax-Free Crypto Activities

Some crypto activities don’t trigger immediate tax obligations. Simply buying and holding crypto doesn’t create a taxable event.

Transferring crypto between wallets you own isn’t taxable. You’re not disposing of the asset, just moving it to a different storage location.

Donating cryptocurrency to registered charities can be exempt from Capital Gains Tax. Always keep records of these charitable transactions.

If you’ve made losses on your crypto investments, you can offset these against other capital gains. You can also offset future gains by carrying forward losses to the same tax year or future years. If your crypto becomes worthless, making a negligible value claim may allow you to realize a loss for tax purposes. This can effectively reduce your overall tax bill.

Consider legal tax strategies to avoid paying tax, such as timely loss claims and professional advice. Good record-keeping is essential to ensure tax compliance.

HMRC Reporting Requirements

You must complete a Self Assessment tax return if your crypto gains exceed the Annual Exempt Amount. It is important to prepare a detailed tax report or crypto tax report that consolidates all your crypto transactions to ensure accurate reporting and easier tax filing.

Keep detailed records of all transactions, including dates and values in pounds sterling. HMRC can request information going back several years.

HMRC is increasingly obtaining information directly from UK-based cryptocurrency exchanges. This makes compliance more important than ever. To ensure tax compliance, keep thorough records and submit accurate tax reports or crypto tax reports as required by HMRC.

Common Crypto Tax Mistakes

Many crypto users forget that trading one cryptocurrency for another counts as a disposal. This can trigger Capital Gains Tax even without converting to pounds. Spending crypto on goods and services is also considered a taxable event in the UK, which can trigger crypto taxes.

Not keeping proper records is another common mistake. Without accurate records, calculating your tax liability becomes nearly impossible.

Some investors incorrectly assume all crypto activities are treated the same. In reality, different activities may trigger different types of tax.

Misunderstanding the cost basis rules for crypto can lead to incorrect calculations. Mistakes in calculating taxable gains can result in underpayment of tax and potential HMRC penalties.

Final Thoughts

Staying compliant with UK crypto tax rules requires understanding when tax obligations arise. Good record-keeping is essential for all your crypto activities.

Most crypto tax liabilities come from Capital Gains Tax when you dispose of assets. Some activities like mining and staking trigger Income Tax instead.

HMRC is paying increasing attention to cryptocurrency compliance. This makes it essential to properly report and pay any taxes due on time.

Even if you're below the tax-free threshold, maintaining records is crucial. HMRC can request information going back several years.

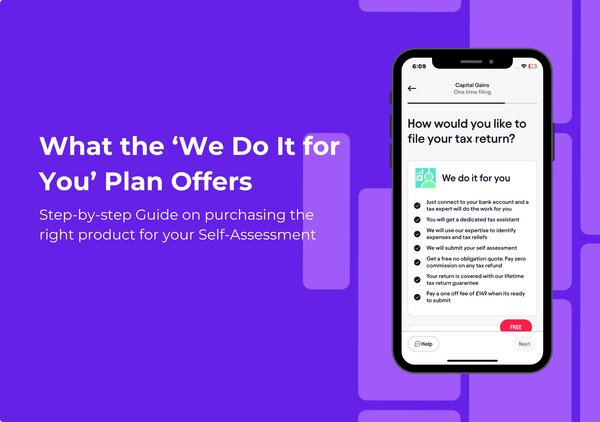

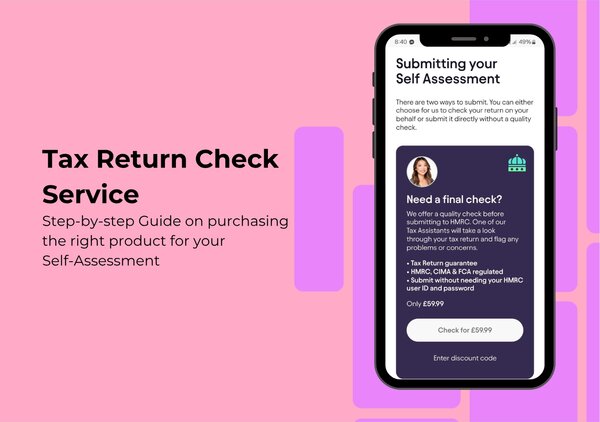

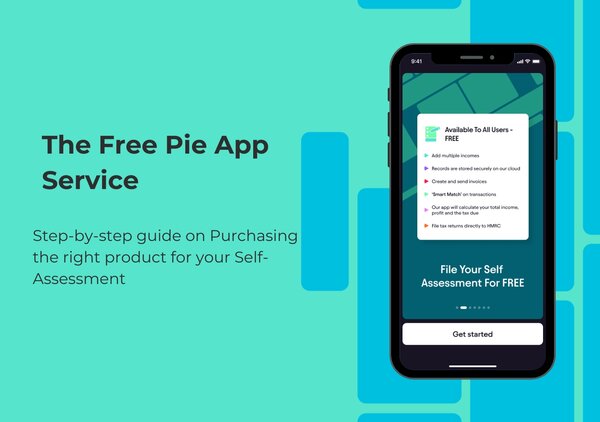

Pie.tax: Simplifying Crypto Tax

Getting your crypto tax right doesn’t have to be a headache, even with complex trading histories.

The UK’s first personal tax app, Pie.tax, automatically imports your transactions from all major exchanges and wallets. It calculates your tax position in real-time as you trade. The app can also generate a comprehensive crypto tax report, making your tax filing process much simpler.

Our dedicated crypto tax assistants understand the nuances of DeFi, staking, and mining taxation. This saves you hours of research and calculations.

All your tax obligations appear on a unified dashboard. This makes it simple to see exactly what you owe and when.

Feel free to explore the Pie.tax app if you’d like to see how it can make your crypto tax reporting straightforward.